When the Paycheck Stops Being Enough

A salary that used to cover the month, and the quiet math when it no longer does.

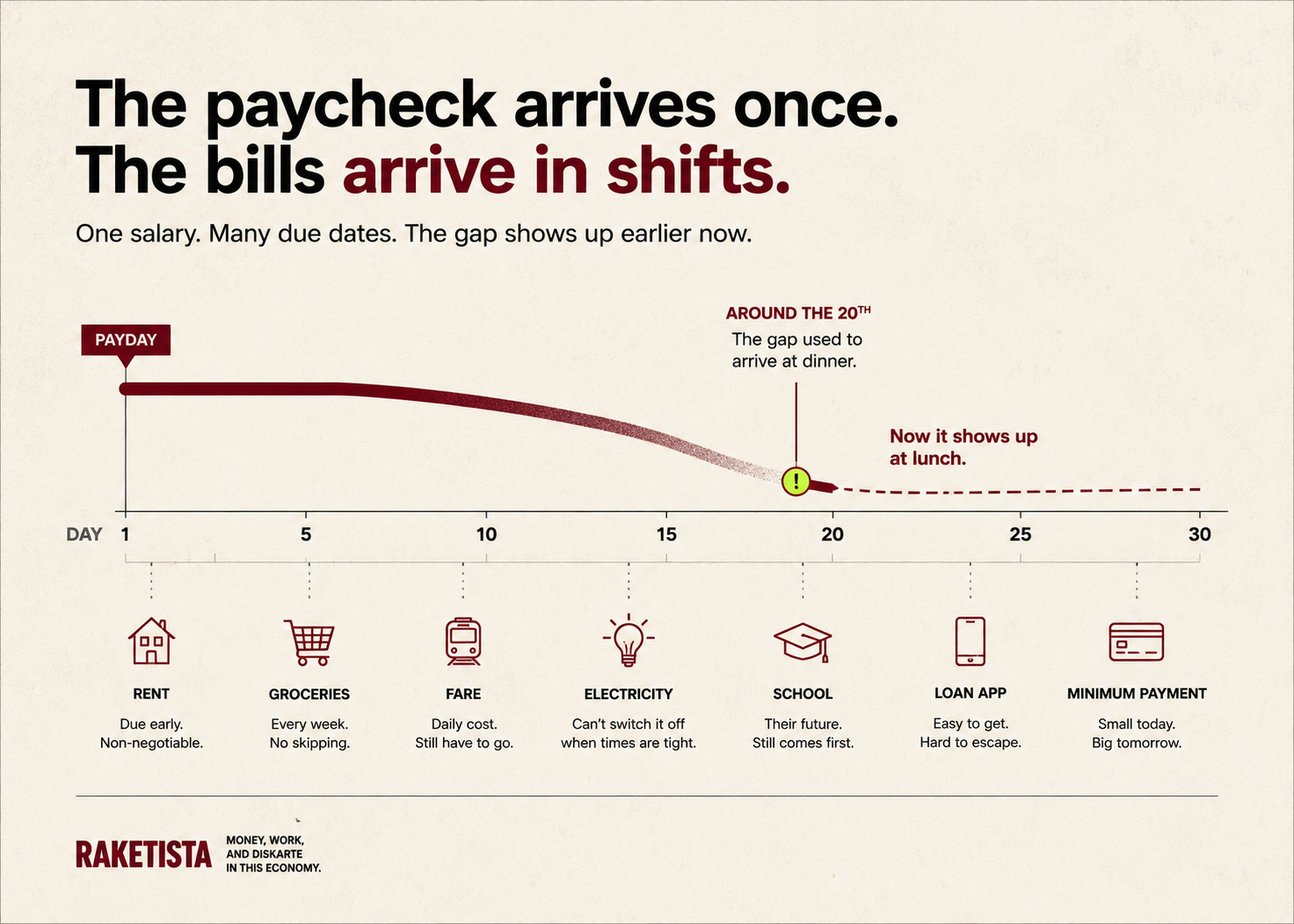

There’s a particular kind of quiet that happens around the 20th of the month.

The salary landed two weeks ago. It was real money. You’re not careless with it, and you’re not lazy — you’ve never been lazy a day in your life. But the math has started doing something it didn’t used to do. The bills are the same bills. The pay is, more or less, the same pay. And somehow the gap between them keeps showing up earlier each month, like a guest who used to arrive at dinner and now turns up at lunch.

Nobody talks about this part out loud. You go to work, you smile, you pay what you can, you move money from one place to cover another. From the outside, nothing is wrong. You have a job. You have a salary. By every official measure, you are fine.

You just don’t feel fine, and you’re not imagining it.

The squeeze is real, and it isn’t your fault

Here’s what’s actually happening, in plain terms.

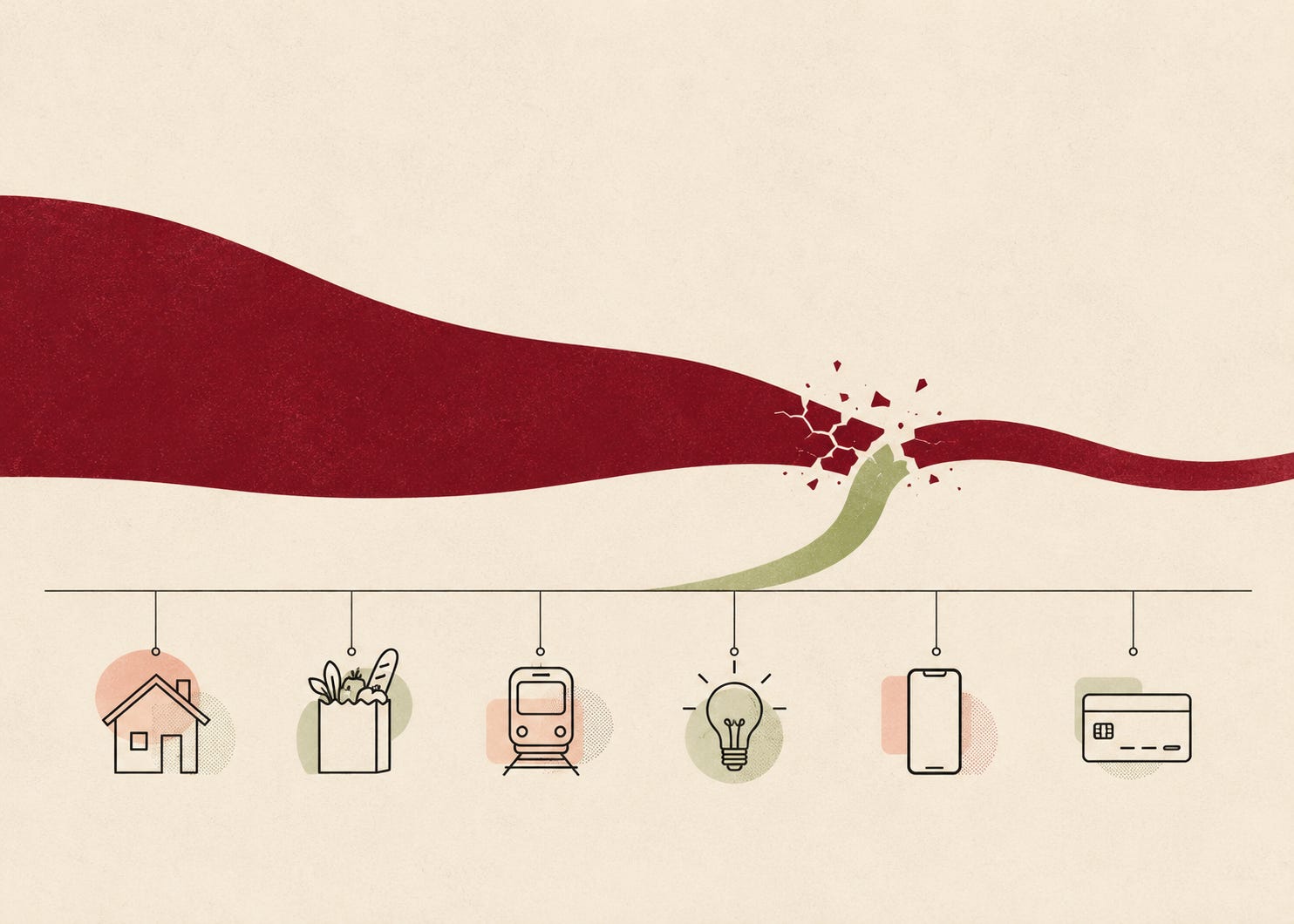

Your salary buys less than it did a few years ago. That’s not a feeling — it’s inflation, and it’s measurable. The same grocery run, the same jeepney fare, the same electric bill: each one quietly costs more, while the number on your payslip stays put or crawls. Economists have a tidy word for this. The rest of us just notice that the money runs out faster and wonder what we did wrong.

The answer is: probably nothing. A salary that comfortably covered a household in 2019 can leave that same household short in 2026, with no change in spending and no new bad habit to blame. The ground moved. You’re standing where you always stood.

And for a lot of people, the gap doesn’t just sit there politely. It gets filled — by a loan app that approves you in four minutes, by a credit card’s minimum payment, by borrowing a little from next month to finish this one. None of these are signs of a weak character. They’re what a reasonable person reaches for when the math doesn’t close and the rent is due. The trouble is that some of those tools are built to make the gap wider, not smaller. We’ll spend a lot of time on those in the months ahead, because they’re the quiet reason a squeeze becomes a spiral.

Why “just spend less” stops working

The usual advice arrives right about now: cut back, budget harder, skip the milk tea.

Sometimes that’s fair. There’s almost always something to trim. But tell it to someone whose income genuinely no longer covers the basics, and you’ve said nothing useful at all. You can’t budget your way out of a gap that exists after the budgeting is done. At some point the problem isn’t the spending. It’s that there’s only one stream of money coming in, and it isn’t enough anymore.

That’s the uncomfortable part, and also, strangely, the freeing one. Because if the problem were really your discipline, the fix would be to become a different, more disciplined person — which is hard, slow, and a little insulting. But if the problem is the structure — one income, rising costs — then the fix is structural too. And structures can be changed.

The squeeze is a problem you can work

This is the whole idea behind RAKETISTA, so it’s worth saying clearly, once.

A squeeze is not a verdict on who you are. It’s a situation. It has moving parts — what comes in, what goes out, what’s quietly eating you from the side. Each of those parts can be understood, and most of them can be moved, even if only a little at a time. You stop the bleeding first. Then you find a second stream of money — a raket — that fits the hours and the skills you already have. Then you protect what you’ve built so the next bad month doesn’t undo it. None of it is magic, and none of it happens in a week. But all of it is workable, which is a very different thing from hopeless.

We’re not here to sell you a dream, or a course, or a mindset that fixes your life if you just believe hard enough. There’s enough of that already, and most of it is noise. What we’re here to do is look at how money and work actually function for ordinary Filipinos right now — honestly, in plain language — and figure out the moves that hold up.

You found this on what was probably not your best financial week. That’s usually when people go looking. The good news is simple, even if the work isn’t: the same math that’s running against you right now will run for you the moment you get ahead of it. Getting ahead of it is the part we can do something about.

Let’s get to work.